FHA Loans in Folsom, CA

Presented by Andrey Dimitrashuk at Lending Concepts

Your Trusted Local FHA Mortgage Expert

Buying a home in Folsom, California, is a major milestone. With its excellent schools, beautiful parks, and proximity to Folsom Lake, it is no surprise that so many families and professionals want to put down roots in this vibrant community. However, navigating the local real estate market and securing the right financing can feel overwhelming. If you are a first-time homebuyer, have a less-than-perfect credit score, or simply want to keep your down payment low, an FHA home loan might be the perfect solution for you.

At Lending Concepts, Andrey Dimitrashuk specializes in helping Folsom residents achieve their homeownership dreams through flexible, affordable FHA home loans. Whether you are looking at a charming property in Historic Folsom, a family home in Broadstone, or a modern build in Empire Ranch, we are here to guide you through every step of the mortgage process.

Ready to explore your mortgage options? Call Andrey Dimitrashuk today at 559-709-1820 or email [email protected] to start your journey.

What is an FHA Home Loan?

An FHA loan is a mortgage insured by the Federal Housing Administration, which is a government agency within the U.S. Department of Housing and Urban Development (HUD). Because these loans are backed by the government, lenders like Lending Concepts can offer them to borrowers with more lenient qualifying requirements compared to conventional mortgages.

FHA loans were specifically designed to make homeownership more accessible to the average American. They are incredibly popular among first-time homebuyers in Folsom, but you do not have to be a first-time buyer to qualify. If you plan to live in the home as your primary residence, an FHA loan offers a secure, fixed-rate or adjustable-rate financing option with highly attractive terms.

Key Benefits of FHA Loans in Folsom, CA

Choosing an FHA loan comes with a variety of unique advantages tailored to help buyers overcome common financial hurdles. When you work with Andrey Dimitrashuk to secure your FHA mortgage, you can expect the following benefits:

Low Down Payment Requirements: One of the biggest obstacles to buying a home in California is saving for a down payment. With an FHA loan, you can purchase a home with a down payment as low as 3.5% of the purchase price.

Flexible Credit Score Guidelines: Conventional loans often require high credit scores to get the best rates. FHA loans are much more forgiving. You can qualify for the 3.5% down payment option with a credit score of 580 or higher. Even if your score is between 500 and 579, you may still qualify with a 10% down payment.

Gift Funds are Allowed: If you do not have enough saved for the 3.5% down payment, the FHA allows 100% of your down payment and closing costs to come from a financial gift. This gift can be from a family member, an employer, or an approved charitable organization.

Higher Debt-to-Income (DTI) Ratios: FHA guidelines are generally more accommodating when it comes to the amount of debt you carry relative to your income. This flexibility makes it easier to get approved even if you have student loans, car payments, or credit card debt.

Seller Concessions: The FHA allows property sellers to contribute up to 6% of the purchase price toward your closing costs, prepaid expenses, and discount points. This can significantly reduce the amount of cash you need to bring to the closing table.

Assumable Mortgages: Most FHA loans are assumable. This means that if you decide to sell your Folsom home in the future, the buyer can take over your FHA loan at your current interest rate. In a rising interest rate environment, this can be a massive selling feature for your property.

FHA Loan Requirements and Eligibility

While FHA loans are designed to be accessible, there are still specific guidelines set by the Federal Housing Administration that borrowers must meet. Andrey Dimitrashuk and the team at Lending Concepts will help you review your financial profile to ensure you meet these criteria.

Basic Borrower Requirements

To qualify for an FHA loan in Folsom, you will need to provide documentation verifying your income, employment history, and identity. Lenders will look at your W-2s, pay stubs, tax returns, and bank statements. You must have a steady employment history or have worked for the same employer for the past two years.

Property Requirements

FHA loans are intended to promote primary homeownership. Therefore, you cannot use an FHA loan to purchase an investment property or a vacation home. You must intend to move into the property within 60 days of closing and live there as your primary residence for at least one year.

Additionally, the property must meet minimum health and safety standards set by HUD. An FHA-approved appraiser will inspect the home to ensure the roof, foundation, electrical, plumbing, and heating systems are in good, safe working order. If the home requires significant repairs, it may not qualify for a standard FHA loan, though an FHA 203(k) renovation loan might be an alternative option.

Eligible Property Types

You might be surprised by the variety of properties you can purchase with an FHA loan in Sacramento County. Eligible properties include:

Single-family detached homes

Townhouses and approved condominiums

Multi-family properties with up to four units (as long as you live in one of the units)

Manufactured homes permanently affixed to a foundation

FHA Loan Limits in Sacramento County

The Federal Housing Administration sets maximum loan limits that vary by county and are adjusted annually based on local home prices. Because Folsom is located in Sacramento County, buyers must adhere to the county specific FHA loan limits. For the most current, up to date FHA loan limits in Folsom, please contact Andrey Dimitrashuk directly, as these figures change yearly to reflect the dynamic California real estate market.

FHA Loans vs. Conventional Loans: Which is Right for You?

Many homebuyers in Folsom weigh the differences between Conventional and FHA loans. Below is a detailed comparison to help you understand why an FHA loan might be the superior choice for your situation.

| Feature | FHA Loan | Conventional Loan |

|---|---|---|

| Minimum Down Payment | 3.5% (with a 580+ credit score) | 3% for first-time buyers, typically 5% to 20% for others |

| Minimum Credit Score | 500 (with 10% down) or 580 (with 3.5% down) | Typically 620 or higher |

| Mortgage Insurance | Upfront Premium (UFMIP) and Annual Premium required for the life of the loan (in most cases) | Private Mortgage Insurance (PMI) required if down payment is less than 20%. Can be canceled later. |

| Property Condition | Must meet strict HUD safety and habitability standards | Generally more lenient on minor property defects |

| Income Limits | No income limits | No income limits (except for certain specialized conventional programs) |

| Loan Limits | Subject to county specific FHA limits | Subject to Federal Housing Finance Agency (FHFA) conforming loan limits |

If you have excellent credit and a larger down payment, a conventional loan might save you money on mortgage insurance. However, if you are building your credit, have a higher debt-to-income ratio, or want to maximize your purchasing power with a smaller down payment, an FHA loan is an outstanding choice. Andrey Dimitrashuk will run the numbers for both options to ensure you get the most cost effective mortgage for your specific situation.

Understanding FHA Mortgage Insurance Premiums (MIP)

Because the FHA insures your loan against default, they require borrowers to pay Mortgage Insurance Premiums (MIP). This insurance is what allows lenders to offer such favorable terms. It is important to understand how this insurance works when budgeting for your Folsom home purchase.

Upfront Mortgage Insurance Premium (UFMIP)

Annual Mortgage Insurance Premium

In addition to the upfront premium, FHA borrowers pay an annual mortgage insurance premium. This premium is divided by 12 and added to your monthly mortgage payment. The exact rate of the annual MIP depends on your loan term, your loan amount, and your loan-to-value (LTV) ratio. For most borrowers putting down 3.5%, the annual premium lasts for the entire life of the loan. However, if you eventually build 20% equity in your home, you have the option to refinance into a conventional loan to eliminate this monthly mortgage insurance payment.

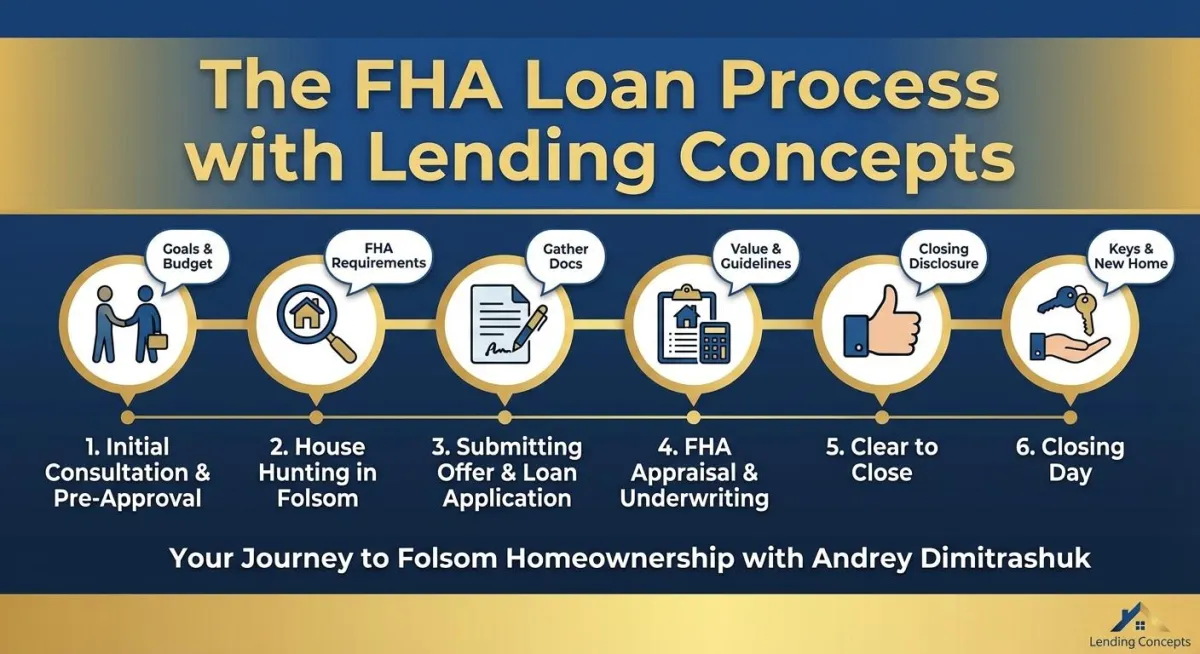

The FHA Loan Process with Lending Concepts

Initial Consultation and Pre-Approval: The process begins with a simple conversation. You will discuss your homeownership goals, budget, and timeline with Andrey. By reviewing your income, assets, and credit, Andrey will provide you with a pre-approval letter. This letter is crucial for showing Folsom real estate agents and sellers that you are a serious, qualified buyer.

House Hunting in Folsom: Armed with your pre-approval, you can confidently search for homes in Folsom and the surrounding Sacramento County areas. Remember to keep FHA property requirements in mind as you view potential homes.

Submitting an Offer and Loan Application: Once you find the perfect home and your offer is accepted, you will officially submit your FHA loan application. Andrey will help you gather the final necessary documents, such as updated bank statements and pay stubs.

FHA Appraisal and Underwriting: Lending Concepts will order an FHA appraisal. The appraiser will determine the fair market value of the home and inspect it to ensure it meets HUD minimum property standards. Simultaneously, our underwriting team will review your file to ensure all FHA guidelines are met.

Clear to Close: Once the underwriter approves your file and the appraisal is cleared, you will receive a "Clear to Close." You will review your Closing Disclosure, which details your final loan terms, monthly payment, and cash needed to close.

Closing Day: You will sign your final mortgage documents, provide your down payment and closing costs, and receive the keys to your new Folsom home.

Why Choose Andrey Dimitrashuk as Your Folsom Mortgage Expert?

The mortgage lender you choose can make or break your home buying experience. As a trusted mortgage professional at Lending Concepts, Andrey Dimitrashuk brings a wealth of local knowledge, financial expertise, and a client-first approach to the table.

Local Market Expertise: Understanding the nuances of the Folsom and Sacramento County real estate markets allows Andrey to structure your loan competitively. He knows what local listing agents look for in a pre-approval and works diligently to make your offer stand out.

Personalized Communication: You are never just a transaction number at Lending Concepts. Andrey takes the time to explain every detail of the FHA loan process, ensuring you feel confident and informed from the first phone call to the closing table.

Problem-Solving Approach: If there are hurdles in your credit history or complexities in your income structure, Andrey has the experience to find solutions. He works proactively to address potential underwriting issues before they become roadblocks.

Speed and Efficiency: In a competitive market like Folsom, speed matters. Andrey and the Lending Concepts team utilize streamlined processes to close your FHA loan on time, every time.

Do not leave your home financing to chance. Partner with a local expert who is invested in your success.

Take the Next Step Toward Homeownership in Folsom

Your dream of owning a home in Folsom, CA, is closer than you think. With the flexible requirements and low down payment options of an FHA loan, homeownership is within reach. Do not navigate the complex mortgage landscape alone. Let Andrey Dimitrashuk and the team at Lending Concepts provide the clarity, strategy, and dedicated service you deserve.

Contact Andrey Dimitrashuk Today:

Phone: 559-709-1820

Email: [email protected]

Business: Lending Concepts

Service Area: Folsom, CA and surrounding areas

Disclaimer: All loans are subject to credit and underwriting approval. Programs, rates, terms, and conditions are subject to change without notice. Lending Concepts is an Equal Housing Lender. Please contact Andrey Dimitrashuk for the most current FHA loan limits, interest rates, and specific qualification requirements.

Frequently Asked Questions About FHA Loans

Can I use an FHA loan to buy a multi-family home in Folsom?

Yes. You can use an FHA loan to purchase a duplex, triplex, or fourplex. The primary requirement is that you must live in one of the units as your primary residence. This is a fantastic strategy for first-time buyers looking to generate rental income to help offset their mortgage payment.

Do I have to be a first-time homebuyer to get an FHA loan?

No. While FHA loans are incredibly popular with first-time buyers due to the low down payment requirements, repeat buyers are fully eligible. As long as the home you are purchasing will be your primary residence, you can apply for an FHA loan.

What happens if the home I want to buy needs repairs?

If the home requires minor cosmetic updates, it will likely pass the FHA appraisal. However, if there are major health and safety issues, such as a failing roof or exposed wiring, the seller must repair these issues before the loan can close. Alternatively, you can explore an FHA 203(k) loan, which allows you to finance both the purchase price and the cost of renovations into a single mortgage.

Can I refinance my current mortgage into an FHA loan?

Yes. FHA offers rate-and-term refinances, cash-out refinances, and a highly streamlined program known as the FHA Streamline Refinance. If you already have an FHA loan, the Streamline program allows you to lower your interest rate with reduced documentation and, in many cases, without a new appraisal.

How long does it take to close an FHA loan?

On average, an FHA loan takes about 30 to 45 days to close from the time you have an accepted purchase contract. Andrey Dimitrashuk works diligently to ensure all paperwork is processed efficiently, often beating industry average closing times.

Ready to Take the Next Step?

If you are thinking about buying, refinancing, or simply want to understand your options, the next step starts with a simple conversation.

No pressure. Just clear answers and a plan.

Get Pre-Approved Online

Schedule a Call with Andrey Today

Andrey Dimitrashuk

Mortgage Loan Originator · DBA: Loans by Drey

Individual NMLS #1583893 | CalDRE #02070049

Lending Concepts

Real Estate Broker — California Department of Real Estate

Company NMLS #1206623 | CalDRE #01957794

Folsom Office (Primary)

785 Orchard Dr #250

Folsom, CA 95630

Clovis Office (Brokerage HQ — by appointment)

565 Pollasky Ave, Suite 201

Clovis, CA 93612

Hours: Open 24 hours

Languages: English · Russian · Ukrainian

Языки: Английский · Русский · Украинский

Мови: Англійська · Російська · Українська

Loan Programs

Conventional Loans

FHA Home Loans

VA Home Loans

USDA Loans

Jumbo Home Loans

Refinance

Reverse Mortgage

Alternative Loans (Non-QM)

Loan Programs

About Drey

FAQ

Reviews

Mortgage Learning Center

Calculators

12-Step Pre-Approval

Blog

Schedule a Call

Company

Contact

Privacy Policy (CCPA)

Accessibility (WCAG 2.1 AA)

We are pledged to the letter and spirit of U.S. policy for the achievement of equal housing opportunity throughout the Nation. We encourage and support an affirmative advertising and marketing program in which there are no barriers to obtaining housing because of race, color, religion, sex, handicap, familial status, or national origin.

License Disclosure

Andrey Dimitrashuk — NMLS #1583893 | CalDRE #02070049. Lending Concepts — NMLS #1206623 | CalDRE #01957794. Licensed in CA. Verify: NMLS Consumer Access · CalDRE. DRE Mortgage Loan Activities: (877) 373-4542.

Not a Commitment to Lend — Regulation Z

This is not a commitment to lend. All applications subject to credit approval, underwriting, appraisal, and title. Programs, rates, and terms subject to change without notice. Not all applicants qualify. Subject to Truth in Lending Act disclosures (12 CFR §1026).

California Consumer Privacy Act

California residents: review our Privacy Policy for information about your rights under the CCPA.

Accessibility — ADA / WCAG 2.1 AA

We are committed to digital accessibility. See our Accessibility Statement for details.

© 2026 Loans by Drey, a DBA of Andrey Dimitrashuk operating under Lending Concepts. All rights reserved.

Last updated: June 2, 2026