by Andrey Dimitrashuk at Lending Concepts

Conventional Loans in Folsom, CA

Welcome to your premier destination for securing conventional loans in Folsom, California. Navigating the real estate market requires a solid financial foundation, and a conventional mortgage is often the most powerful tool for homebuyers. Whether you are purchasing your first home, upgrading to a larger space for your growing family, or investing in Folsom real estate, Andrey Dimitrashuk and the team at Lending Concepts are here to guide you every step of the way.

With a commitment to transparent communication, competitive rates, and personalized financial strategies, we make the mortgage process seamless. Discover how a conventional loan can help you unlock the doors to your dream home in Folsom.

Conventional Loans in Folsom, CA

Presented by Andrey Dimitrashuk at Lending Concepts

Trusted by these Partners

Your Trusted Local Conventional Mortgage Expert

Welcome to your premier destination for securing conventional loans in Folsom, California. Navigating the real estate market requires a solid financial foundation, and a conventional mortgage is often the most powerful tool for homebuyers. Whether you are purchasing your first home, upgrading to a larger space for your growing family, or investing in Folsom real estate, Andrey Dimitrashuk and the team at Lending Concepts are here to guide you every step of the way.

With a commitment to transparent communication, competitive rates, and personalized financial strategies, we make the mortgage process seamless. Discover how a conventional loan can help you unlock the doors to your dream home in Folsom.

What is a Conventional Loan?

A conventional loan is a type of mortgage that is not insured or guaranteed by a government agency, such as the Federal Housing Administration (FHA), the Department of Veterans Affairs (VA), or the United States Department of Agriculture (USDA). Instead, conventional loans are backed by private lenders and often sold to government-sponsored enterprises known as Fannie Mae and Freddie Mac.

Because the government does not back these loans, they typically require a slightly higher credit score and a lower debt-to-income ratio compared to government-backed mortgages. However, conventional loans offer incredible flexibility, highly competitive interest rates, and a wide variety of terms that make them the most popular choice among homebuyers in Folsom and across the nation.

Conforming vs. Non-Conforming Conventional Loans

Conventional loans are generally categorized into two main types: conforming and non-conforming.

Conforming Loans: These loans adhere to the strict guidelines and borrowing limits set by Fannie Mae and Freddie Mac. The Federal Housing Finance Agency (FHFA) adjusts these loan limits annually based on average home prices. In Folsom, which is located in Sacramento County, conforming loan limits are generous, allowing buyers to purchase standard single-family homes with ease.

Non-Conforming Loans: Also known as Jumbo Loans, these mortgages exceed the maximum loan limits established by the FHFA. If you are looking to purchase a luxury property in Folsom that requires a loan amount higher than the conforming limit, a non-conforming jumbo loan would be the appropriate conventional financing option.

The Benefits of Choosing a Conventional Mortgage in Folsom

When you work with Andrey Dimitrashuk at Lending Concepts, we take the time to evaluate your unique financial situation to determine if a conventional loan is your best path forward. For many borrowers, the benefits are substantial.

1. Flexible Down Payment Options

A common myth in real estate is that you must have a 20 percent down payment to purchase a home. In reality, conventional loans offer highly flexible down payment options. First-time homebuyers may qualify for a conventional loan with a down payment as low as 3 percent. Repeat buyers can often secure a conventional loan with just 5 percent down. This flexibility allows you to keep more of your savings for home improvements, furnishings, or emergency funds.

2. No Upfront Mortgage Insurance Fees

Unlike FHA loans, which require an upfront mortgage insurance premium at closing, conventional loans do not charge an upfront mortgage insurance fee. If you put down less than 20 percent, you will be required to pay Private Mortgage Insurance (PMI), but this is paid monthly and can be removed later.

3. Cancellable Private Mortgage Insurance (PMI)

One of the most significant financial advantages of a conventional loan is the ability to cancel your PMI. Once you reach 20 percent equity in your home, either through paying down your principal balance or through home value appreciation in the robust Folsom real estate market, you can request to have your PMI removed. This instantly lowers your monthly mortgage payment. FHA loans, by contrast, often require mortgage insurance for the life of the loan if you put down less than 10 percent.

4. Versatile Property Types

Conventional loans are incredibly versatile. While government-backed loans are strictly for primary residences, conventional financing can be used for a variety of property types. You can use a conventional loan to finance a primary residence, a vacation home, or an investment property in Folsom.

5. Stronger Offers in a Competitive Market

Folsom is a highly desirable place to live. In a competitive housing market, sellers often prefer buyers who are pre-approved for conventional loans. Conventional appraisals are generally less stringent regarding minor property repairs compared to FHA or VA appraisals. By securing a conventional loan pre-approval with Lending Concepts, your offer will stand out to sellers and listing agents.

Conventional Loan Requirements in Folsom, CA

To qualify for a conventional loan, borrowers must meet specific financial criteria. Andrey Dimitrashuk will help you review your financial profile to ensure you meet these standard requirements.

Credit Score Expectations

Credit scores play a vital role in conventional lending. While the absolute minimum credit score required for a conventional loan is typically 620, borrowers with higher credit scores will unlock the best interest rates and the lowest PMI premiums. A score of 740 or above is generally considered excellent and will yield the most favorable loan terms.

Debt-to-Income (DTI) Ratio

Your DTI ratio represents the percentage of your gross monthly income that goes toward paying your monthly debts. Lenders use this metric to ensure you can comfortably manage your new mortgage payments. For conventional loans, a DTI of 36 percent or lower is ideal, though many conventional programs allow a DTI of up to 45 percent, and sometimes up to 50 percent with strong compensating factors like a high credit score or substantial cash reserves.

Employment and Income Verification

Stable employment is crucial. Lenders typically look for a two-year history of consistent employment and income. When you apply, you will need to provide recent pay stubs, W-2 forms, and tax returns. If you are self-employed, Andrey Dimitrashuk specializes in helping entrepreneurs navigate the documentation needed to prove income stability for conventional financing.

Down Payment and Reserve Funds

As mentioned, down payments can range from 3 percent to 20 percent or more. Additionally, lenders want to see that the funds for your down payment and closing costs have been "seasoned" meaning they have been sitting in your bank account for at least 60 days. You may also need to show that you have a few months of mortgage payments in reserve, particularly if you are buying an investment property.

Fixed-Rate vs. Adjustable-Rate Conventional Mortgages

When structuring your conventional loan with Lending Concepts, you will have the choice between a fixed-rate mortgage and an adjustable-rate mortgage (ARM). Andrey Dimitrashuk provides expert advice to help you choose the right structure based on your long-term financial goals.

Fixed-Rate Conventional Loans

A fixed-rate mortgage locks in your interest rate for the entire life of the loan. The most common terms are 15-year and 30-year mortgages, though 20-year terms are also available.

30-Year Fixed: Offers the lowest monthly payment, making it easier to qualify and providing maximum monthly cash flow flexibility.

15-Year Fixed: Features a higher monthly payment but a significantly lower interest rate. This option allows you to build equity rapidly and save tens of thousands of dollars in interest over the life of the loan.

Fixed-rate loans provide peace of mind because your principal and interest payments will never change, protecting you from future interest rate hikes.

Adjustable-Rate Mortgages (ARMs)

An ARM typically starts with a lower interest rate than a fixed-rate mortgage for an initial period, usually 5, 7, or 10 years. After this initial fixed period, the interest rate adjusts annually based on broader market indexes. An ARM can be an excellent strategy if you plan to sell the home or refinance before the initial fixed period expires, allowing you to take advantage of lower initial monthly payments.

Comparing Loan Options: Conventional vs. FHA

Many homebuyers in Folsom weigh the differences between Conventional and FHA loans. Below is a detailed comparison to help you understand why a conventional loan might be the superior choice for your situation.

| Feature | Conventional Loan | FHA Loan |

|---|---|---|

| Minimum Down Payment | 3% (for qualified first-time buyers) | 3.5% |

| Minimum Credit Score | Typically 620 | 580 (for 3.5% down) |

| Mortgage Insurance | PMI required if down payment is under 20%. Can be cancelled later. | Upfront premium required. Annual premium required for the life of the loan (if putting down less than 10%). |

| Property Types allowed | Primary, Second Home, Investment Property | Primary Residence only |

| Appraisal Standards | Standard property condition requirements | Stricter health and safety property requirements |

Note: Loan terms and conditions are subject to change based on market conditions and individual borrower qualifications. Contact Andrey Dimitrashuk for a personalized quote.

The Folsom, CA Real Estate Market

Choosing to buy a home in Folsom, CA is a brilliant investment in your future. Nestled in Sacramento County, Folsom is renowned for its exceptional quality of life, outstanding public schools, and breathtaking outdoor recreation. Securing a conventional loan positions you perfectly to buy into this highly sought-after community.

Why Homebuyers Love Folsom

Folsom Lake and Recreation: Residents enjoy unparalleled access to Folsom Lake State Recreation Area, perfect for boating, paddleboarding, hiking, and cycling along the famous American River Bike Trail.

Top-Tier Education: The Folsom Cordova Unified School district boasts some of the highest-rated schools in the region, making it a prime destination for families.

Historic Charm and Modern Amenities: From the charming boutiques and restaurants in Historic Folsom to the premier shopping at the Palladio at Broadstone, Folsom offers a perfect blend of history and modern convenience.

Strong Property Values: Folsom real estate has historically shown strong appreciation. Buying a home here with a conventional loan is an excellent way to build long-term wealth through home equity.

Navigating Folsom Neighborhoods

Whether you are looking at the luxury estates in Empire Ranch, the family-friendly streets of Broadstone, the established charm of Lexington Hills, or the modern developments south of Highway 50, Andrey Dimitrashuk understands the local market dynamics. A strong conventional pre-approval letter from Lending Concepts ensures that when you find the perfect home in your desired Folsom neighborhood, your offer will be taken seriously by sellers.

Your Step-by-Step Conventional Loan Process in Folsom

At Lending Concepts, we believe that an educated borrower is an empowered borrower. Andrey Dimitrashuk has streamlined the conventional loan process to eliminate stress and ensure a smooth path to the closing table. Here is what you can expect when you partner with us.

Step 1: The Initial Consultation

Step 2: Securing Your Pre-Approval

Before you start touring homes in Folsom, you need a pre-approval letter. We will collect your financial documents, such as tax returns, W-2s, and bank statements. Once reviewed, we will issue a formal pre-approval letter. This document proves to real estate agents and sellers that you are a qualified buyer with reliable conventional financing backing you.

Step 3: House Hunting and Submitting an Offer

Step 4: Loan Processing and Appraisal

Once your offer is accepted, the property goes into escrow, and our processing team takes over. We will lock in your interest rate and order a professional appraisal to confirm the home's market value. During this time, we may ask for updated pay stubs or bank statements to ensure your financial profile remains unchanged.

Step 5: Underwriting Approval

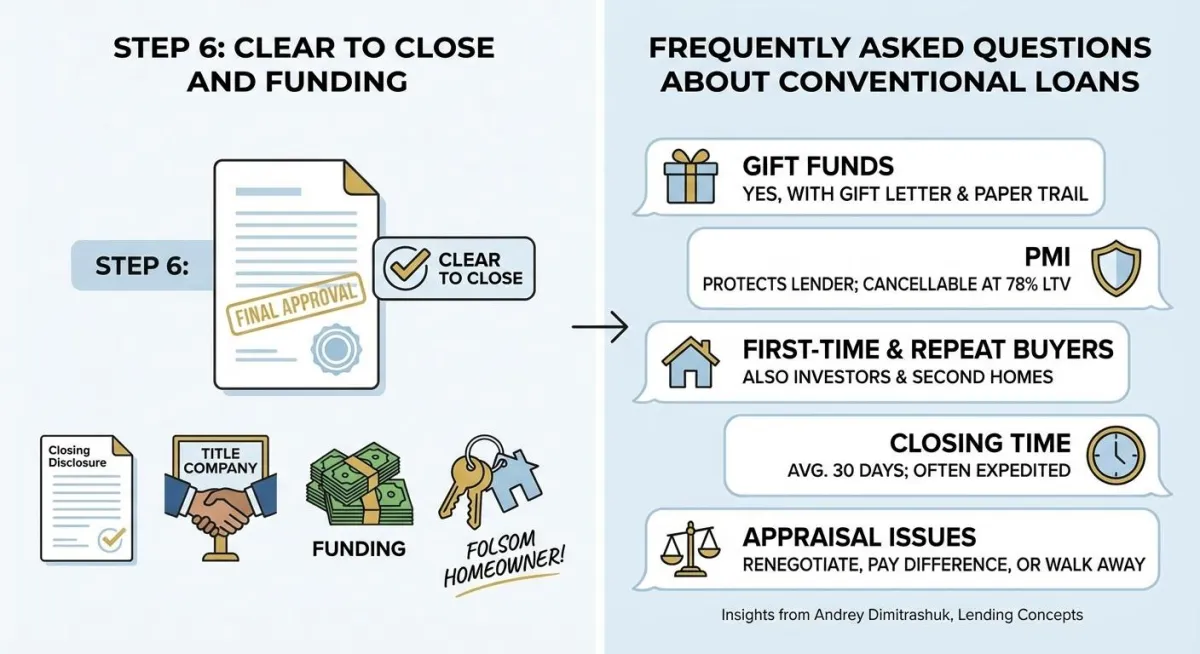

Step 6: Clear to Close and Funding

Once the underwriter gives the final approval, you will receive a "Clear to Close" status. We will provide you with a Closing Disclosure detailing your final loan terms and closing costs. You will sign your final loan documents at a title company, provide your down payment funds, and the loan will be funded. Congratulations, you are now a Folsom homeowner!

Why Choose Andrey Dimitrashuk and Lending Concepts?

Securing a mortgage is one of the most significant financial transactions of your life. You deserve a mortgage advisor who acts as a true fiduciary, putting your best interests first. Here is why Folsom residents trust Andrey Dimitrashuk at Lending Concepts.

Local Expertise: We understand the Folsom real estate market inside and out. We know what sellers expect and how to structure your conventional loan to make your offer the winning one.

Personalized Strategy: You are not just a transaction to us. Andrey takes the time to understand your short-term needs and long-term wealth-building goals, tailoring a mortgage solution that perfectly aligns with your life.

Transparent Communication: The mortgage process can feel overwhelming, but we remove the stress through proactive, clear, and honest communication. You will never be left wondering where your loan stands.

Competitive Rates: As mortgage experts, we have access to top-tier conventional loan products, ensuring you receive highly competitive interest rates and low closing costs.

Ready to Secure Your Conventional Loan in Folsom?

Your dream home in Folsom is within reach. Whether you are ready to apply for a conventional loan today or you simply have questions about your financial readiness, Andrey Dimitrashuk is here to help.

Do not let the complexities of mortgage financing hold you back. Partner with a local expert who is dedicated to your success. Contact Lending Concepts today to schedule your free, no-obligation mortgage consultation.

Contact Information

Andrey Dimitrashuk

Lending Concepts

Phone: 559-709-1820

Email: [email protected]

Service Area: Proudly serving Folsom, CA, and the surrounding communities.

Take the first step toward homeownership in Folsom. Call Andrey Dimitrashuk at Lending Concepts today and discover the power of a conventional mortgage tailored just for you.

Frequently Asked Questions About Conventional Loans

Can I use gift funds for my down payment on a conventional loan?

Yes, conventional loans do allow the use of gift funds for your down payment and closing costs. The gift must come from an acceptable donor, typically a family member. You will need to provide a "gift letter" stating that the funds do not need to be repaid, along with a paper trail showing the transfer of funds from the donor to your account.

How does Private Mortgage Insurance (PMI) work?

If your down payment is less than 20 percent, the lender requires PMI to protect them in case of default. The cost of PMI varies based on your credit score and the size of your down payment. Unlike FHA loans, conventional PMI automatically falls off when your loan balance reaches 78 percent of the home's original purchase price. You can also proactively request cancellation once you reach 20 percent equity through home appreciation or extra principal payments.

Are conventional loans only for first-time homebuyers?

Not at all. While there are excellent 3 percent down conventional programs tailored specifically for first-time buyers, conventional loans are available to repeat buyers, real estate investors, and those looking to purchase second homes or vacation properties.

How long does it take to close a conventional loan in Folsom?

On average, it takes about 30 days from the time your purchase contract is accepted to the day you close. However, Andrey Dimitrashuk and the team at Lending Concepts are known for their efficiency and can often expedite the process if you need a faster closing to win a competitive bid.

What happens if the home appraises for less than the purchase price?

If the appraisal comes in lower than the agreed-upon purchase price, you have a few options. You can renegotiate the price with the seller, pay the difference out of pocket in cash, or walk away from the deal if you have an appraisal contingency in your contract. Andrey will help you navigate this situation closely with your real estate agent.

Ready to Take the Next Step?

If you are thinking about buying, refinancing, or simply want to understand your options, the next step starts with a simple conversation.

No pressure. Just clear answers and a plan.

Get Pre-Approved Online

Schedule a Call with Andrey Today

Andrey Dimitrashuk

Mortgage Loan Originator · DBA: Loans by Drey

Individual NMLS #1583893 | CalDRE #02070049

Lending Concepts

Real Estate Broker — California Department of Real Estate

Company NMLS #1206623 | CalDRE #01957794

Folsom Office (Primary)

785 Orchard Dr #250

Folsom, CA 95630

Clovis Office (Brokerage HQ — by appointment)

565 Pollasky Ave, Suite 201

Clovis, CA 93612

Hours: Open 24 hours

Languages: English · Russian · Ukrainian

Языки: Английский · Русский · Украинский

Мови: Англійська · Російська · Українська

Loan Programs

Conventional Loans

FHA Home Loans

VA Home Loans

USDA Loans

Jumbo Home Loans

Refinance

Reverse Mortgage

Alternative Loans (Non-QM)

Loan Programs

About Drey

FAQ

Reviews

Mortgage Learning Center

Calculators

12-Step Pre-Approval

Blog

Schedule a Call

Company

Contact

Privacy Policy (CCPA)

Accessibility (WCAG 2.1 AA)

We are pledged to the letter and spirit of U.S. policy for the achievement of equal housing opportunity throughout the Nation. We encourage and support an affirmative advertising and marketing program in which there are no barriers to obtaining housing because of race, color, religion, sex, handicap, familial status, or national origin.

License Disclosure

Andrey Dimitrashuk — NMLS #1583893 | CalDRE #02070049. Lending Concepts — NMLS #1206623 | CalDRE #01957794. Licensed in CA. Verify: NMLS Consumer Access · CalDRE. DRE Mortgage Loan Activities: (877) 373-4542.

Not a Commitment to Lend — Regulation Z

This is not a commitment to lend. All applications subject to credit approval, underwriting, appraisal, and title. Programs, rates, and terms subject to change without notice. Not all applicants qualify. Subject to Truth in Lending Act disclosures (12 CFR §1026).

California Consumer Privacy Act

California residents: review our Privacy Policy for information about your rights under the CCPA.

Accessibility — ADA / WCAG 2.1 AA

We are committed to digital accessibility. See our Accessibility Statement for details.

© 2026 Loans by Drey, a DBA of Andrey Dimitrashuk operating under Lending Concepts. All rights reserved.

Last updated: June 2, 2026